22 min read • Energy, Utilities & Resources

The evolution of the street lighting market

What is its role in smart city development?

Executive Summary

The street lighting market is growing globally, boosted by regulatory policies that encourage energy efficiency, IoT convergence, LED price drops, and a new business model “as a service” in different industries. The new concept of “smart poles” is also growing around the world, with use cases that range from basic LED replacement and remote control to the more innovative concept of “smart poles” equipped to offer video surveillance services, air quality monitoring, fiber or Wi-fi connectivity (e.g., Enel’s JuiceLamp).

Public lighting infrastructure has three key features that position itself as potential strategic assets for smart cities’ concept, enabling the development of a common platform with significant cost synergies: capillarity, electrification and connectivity.

This study aims to analyze the main smart city services that can be developed leveraging public lighting infrastructure, identifying the main bottlenecks and roadblocks that prevent large-scale deployment and developing key recommendations for companies entering this new market. In order to do this, we analyzed a number of relevant use cases and interviewed different players along the value chain (Enel X, TIM, Open Fiber, Axxon, Arianna LED and two Italian municipalities). The main findings are summarized below:

- Lighting poles represent a strategic infrastructure for smart city development (and, in particular, for video-surveillance services and autonomous driving) thanks to their capillarity, connectivity and electrification.

- A significant number of pilot projects are emerging in many countries, but with a lack of large-scale deployment.

- The main constraints for large-scale development are related to a demand not yet in place (players need to create demand for smart services, and this takes time), main buyers (public administration) that have financial constraints and lack technical expertise, and the presence of several stakeholders that need to find the right way to collaborate.

- Public lighting operators need to innovate and push on technology innovation and new business models/partnerships to effectively leverage their infrastructure and participate in this new competition area.

1

Market overview and key drivers

Demand

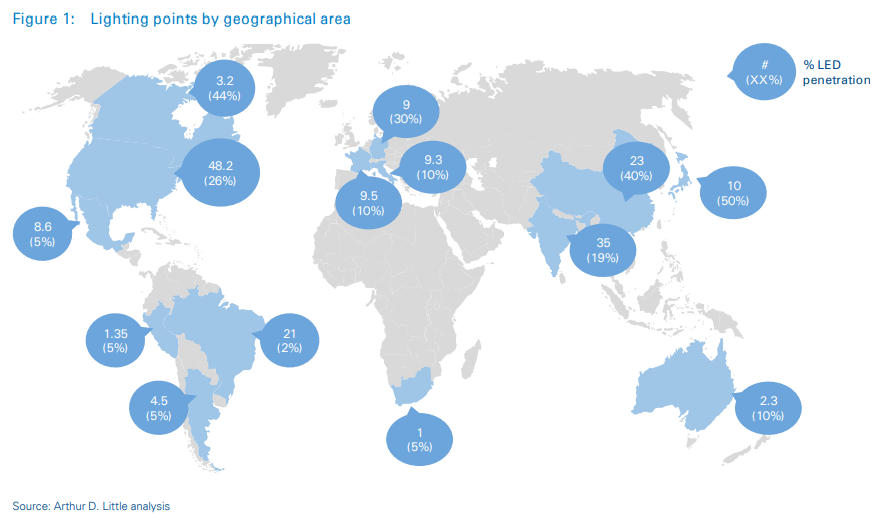

Worldwide, there are around 320 million street lighting poles, with Asia accounting for 25 percent, Europe and North America for 20 percent and South America for 10 percent. Countries and municipalities differ in terms not only of sizing, but also LED penetration, capillarity and business models. The market is driven by several factors, among which are regulatory policies, IoT convergence, and LED price, in addition to the culture and morphology of each area.

Worldwide lighting density, in terms of urban population for each lighting point, is on average around 13, ranging from 7 European countries to over 20 in Asia-Pacific.

As of today, average LED penetration at a global level is still below 15 percent, with significant differences among countries. For example, Japan and Canada showed higher LED penetration rates (around 44-50 percent), while South America showed an average rate below 5 percent.

In Europe penetration is around 10 percent, with only Germany above, and in USA around 26 percent. Even within the same countries, LED penetration are quite different: some big cities have already reached 100 percent (e.g., Milan and New York), while small ones are still struggling, mainly with financial barriers.

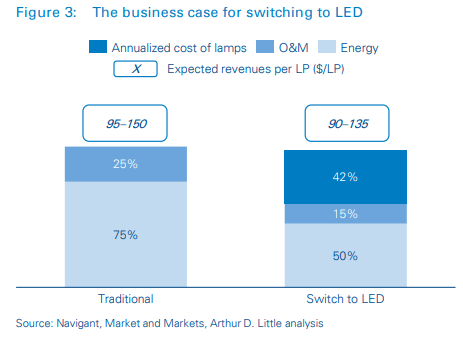

The business case for switching to LED is already strong, as LED technology can generate savings of 50–80 percent of energy costs (which accounts for around 75 percent of total cost, while the other 25 percent is related to O&M).

This allows payback of the initial investment and generation of enough profits to cover the annual cost of lamp replacement.

Key drivers

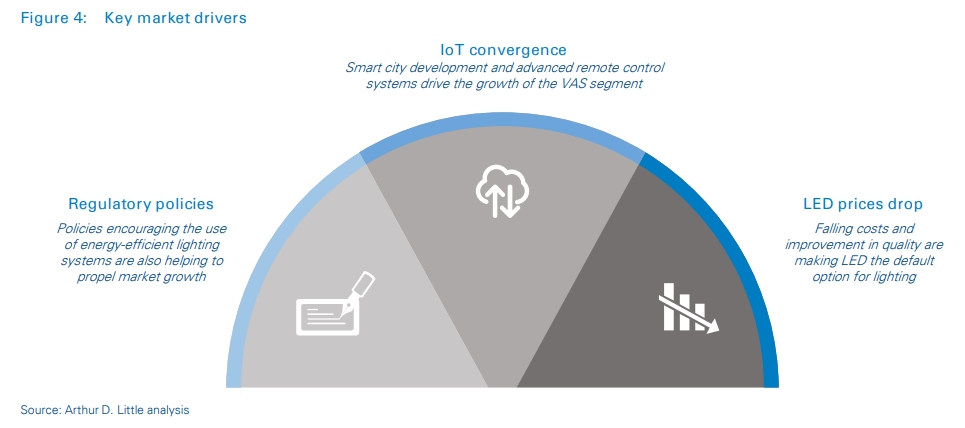

Our study shows three key drivers which are boosting the development of smart street lighting:

- Regulatory policies: Policies encouraging the use of energyefficient lighting systems are also helping to propel market growth

- IoT convergence: Smart city development and advanced remote control systems drive the growth of the VAS segment.

- LED prices drop: Falling costs and improvement in quality are making LED the default option for lighting.

We asked Arianna LED – an Italian company specializing in the design and manufacture of LED lighting systems – what were the main constraints that players faced in “LED transitions” and why the transition process is slow:

- Complex regulation, with several entities engaged.

- Project sizing: a profitable business case requires a minimum of 20,000 street lighting points – potentially attractive to an energy service company (ESCo) aimed at mitigating municipalities’ upfront financial constraints.

- Political conflicts that prevent municipalities from collaborating to organize tenders and benefit from scale.

- Product requirements.

A recommended solution for small municipalities is to pool their decision-making and purchasing power in order to leverage economies of scale and access competitive LED replacement business cases (e.g., as 35 municipalities in southeastern Pennsylvania have done).

Regulatory policies

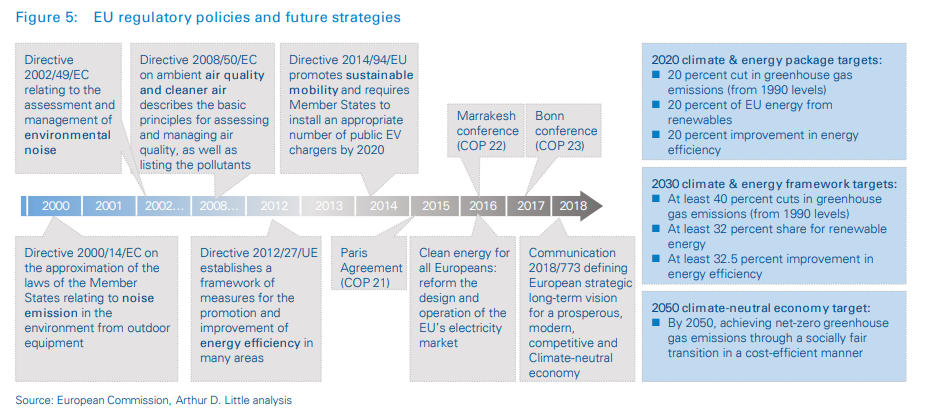

Smart street lighting projects represent a fast and relatively simple way to pursue emission and energy efficiency targets.

At the United Nations Climate Change Conference (COP 21) in Paris in December 2015, 195 countries adopted the first-ever universal, legally binding global climate deal. The agreement set out a global action plan to put the world on track to avoid dangerous climate change by limiting global warming to well below 2°C. To achieve this, the world must stop the growth in greenhouse gas emissions by 2020 and reduce them by 60 percent of 2010 levels by 2050. Furthermore, in 2016 the European Union published the Clean Energy for All Europeans rules, or so-called “Winter Package”, for reforming the European Union electricity market.

Since 2000 Europe has issued many directives about pollution, and after the Paris Agreement it developed different long-term plans, which included increasing targets in 2020, 2030 and 2050. 20 percent of the whole EU budget for 2014-2020 is spent on climate- related actions and the Commission has proposed raising this share to at least 25% for 2021-2027. In addition, on October 3, 2018 the European Parliament voted for a 20 percent cut in CO2 emissions from new cars and vans in 2025, as well as a 40 percent reduction in 2030, in a bid to speed up Europe’s electric car revolution. At the end of 2018, the European Commission defined a vision for a modern, competitive, prosperous and climate-neutral economy, aiming at achieving net-zero greenhouse gas emissions by 2050 through a socially fair, cost-efficient transition (Comm. 773/2018).

In 2017 the US administration decided unilaterally to stay out of the Paris Agreement. The US is one of the very few large, energy-consuming economies that do not have national energy reduction targets in place, although it has adopted stringent energy codes for new buildings.

Canada showed strong commitment to GHG emission reduction with a target of 17 percent below 2005 levels by 2020 and 30 percent by 2030, equivalent to 607 megatons as defined by Canada’s original 2005 baseline. In addition, several energy efficiency initiatives have been defined at either province or federal level on a sector-by-sector basis.

Other local or national initiatives have been promoted by several countries in the far east and Asia, setting ambitious targets in terms of energy efficiency.

South Korea’s second National Energy Master Plan established a goal of 13 percent below the business-as-usual emission level by 2035. It also implemented various regulations, including a plan for an emissions-trading system (financial support and tax credits).

China launched many initiatives in the run-up to COP 21, and developed its climate diplomacy, showing strong improvement in terms of energy intensity. This included a new emission trading system aimed at reducing carbon, which should be up and running in 2019.

IoT convergence

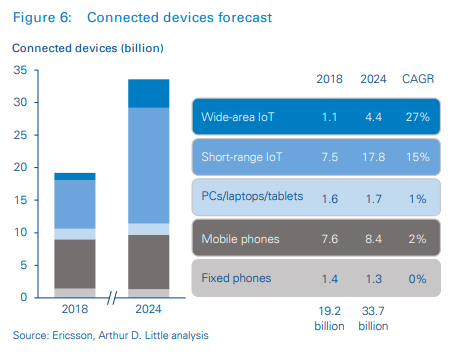

The Internet of Things is the connection of everyday products such as cars, alarm clocks, and lights to computing devices via the internet to allow them to exchange data. Street lighting will benefit from this, as lighting poles will become hosting infrastructure for several connected devices (e.g., sensors, video cameras, EV chargers)

As reported in Figure 6, in 2024 there will be 22 billion connected IoT devices, with an average IoT devices CAGR (wide-area and short-range) of 17 percent.

LED prices drop

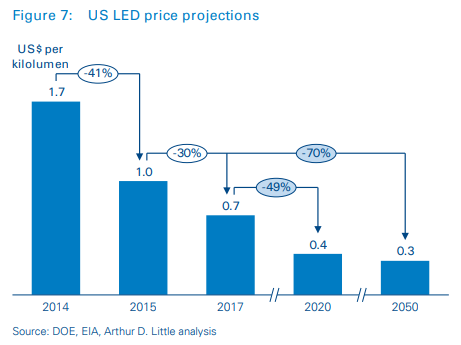

LED prices are expected to strongly decrease in the medium to long term (up to 70 percent by 2050 for USA as reported in Figure 7) and high-quality products (e.g., RGB W) which are able to provide different light temperatures and new services (e.g., adaptive lighting) have been placed on the market.

Value chain and main players

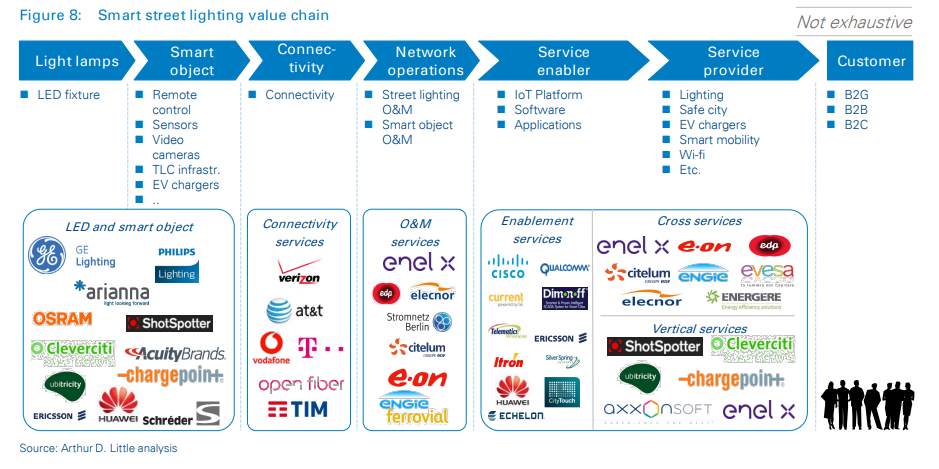

Technology is deeply changing the lighting market, making it into a new booster/enabler for smart city development. However, as a consequence, complexity of the sector’s value chain is increasing and new players are entering the market, as reported in Figure 8.

Utilities typically manage public lighting services, acquiring light lamps from manufacturers, developing O&M services, and defining service-level agreements and related remuneration with municipalities. Now the value chain is changing, with new players entering the market and new partnerships arising. (These include, for example, telco operators that provide connectivity; LED manufactures that, in addition to lamps, are developing their own IOT platforms; vertical players that provide solutions such as EV charging stations and video surveillance services).

Enel X is a global company belonging to the Enel Group with a long-standing experience in installation, operation and maintenance of traditional public lighting. The company is currently focusing its efforts on transitioning the existing asset base to more efficient technology, as well as providing technologically and digitally advanced solutions to B2G customers (municipalities and the like) to support a ‘smart’ urban environment in key application areas in public lighting, mobility, fiber optic-based connectivity, and urban resilience.

As a perfect example of technology integration, efficiency and innovation, Enel X has developed Juice Lamp, an innovative product that combines the latest available lighting technology with two chargers for electric vehicles. The design is attractive and can be adapted to any urban context thanks to its 4 differentiated pole styles.

Features:

- LED light pole combined with remote controlling technology and option to install adaptive lighting features.

- Two integrated chargers with capacity of up to 22kW each, by no means equal to the public standing technology offered by Enel X.

Benefits:

- It can be fitted to any street environment thanks to its range of heights, colors and design: there are 3 ‘modern’ styles plus a ‘classic’ one that fits well within historic sections of cities, or for towns with a specific sensitivity in this area.

- Quick charging, thanks to the Juice Box connectors which each have a capacity of 22kW.

- Interoperability with other potential mobility service providers and possibility to couple any street lighting devices.

- Possibility to integrate video surveillance, traffic analytics, environmental monitoring, connectivity, other smart services.

Scope

With no specific constraint or limitation to its implementation, Enel X has also developed an innovative tool ‘YoUrban©’, a single platform with a twofold application: a mobile app for city-based individuals and a web-based management tool for municipalities.

YoUrban© allows individuals to promptly and easily alert municipalities about lighting points malfunctioning (whose identification is easy thanks to a GPS system) while following any ensuing development, sharing the positive outcome of the maintenance activities on social media, getting access to a section including ‘news’ and earn rewarding points that can be utilized following instructions included in the app.

At the same time, municipalities get an advantage in terms of faster and more cost-effective management of maintenance activities given that the portal allows a fully digitalized experience of activities like, amongst others: i) getting dashboards showing the most relevant key performance indicators about the level of quality of the public lighting system; ii) monitoring of closed/open incidents for urgent interventions, iii) visualization ‘on map’ of the assets under management and customizable statistics about the number of reported incidents, average closing time, etc., iv) direct connection with any related call center and engineers; v) direct connection with suppliers and option to accept online offers and cost estimations for the maintenance and repair activities offered by Enel X.

2

The smart revolution

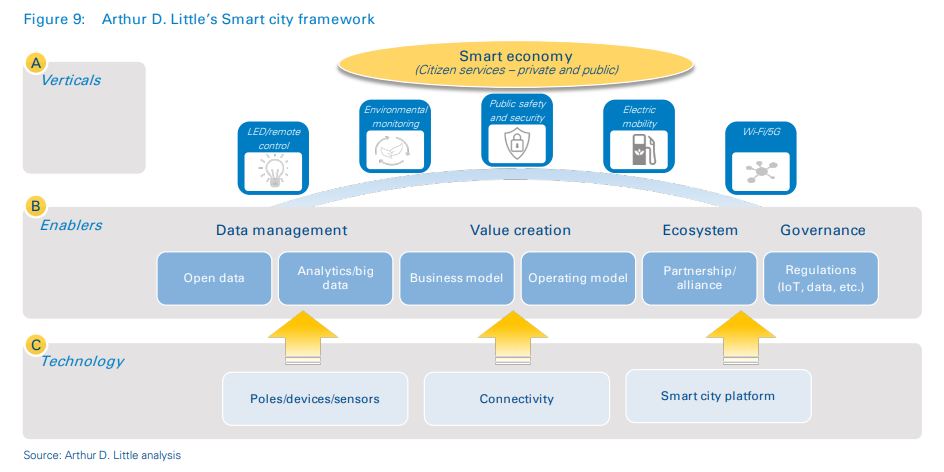

Public lighting infrastructure has three key features that position it as a potential strategic asset for smart city development: capillarity, electrification and connectivity.

Finding new revenue streams implies clear understanding of enablers, constraints and a successful business model.

Arthur D. Little’s “Smart city framework” includes the key pillars to help municipalities leverage their street lighting infrastructure to successfully set up and implement strategies that will transform them into smart cities.

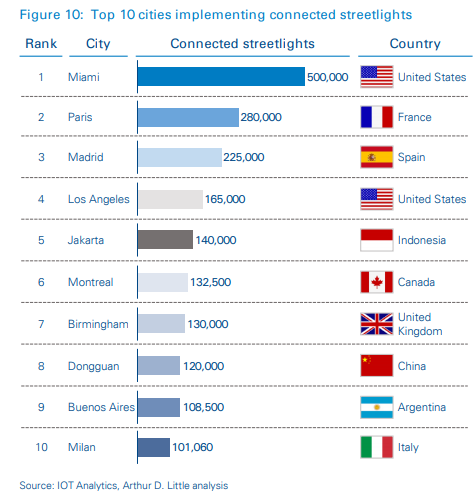

Several cities have already implemented connected LED streetlights using different technologies depending on the smart city’s applications. (Examples include the IEEE 802.15.4g wireless RF mesh architecture used in Miami and Paris, as well as the combination of Vodafone machine-to-machine SIM cards with Vodafone’s M2M wireless network, which was adopted in Los Angeles and Jakarta.)

One of the main infrastructure challenges is to balance the network capacity requirement against the different smart city applications (cost of network roll-out versus benefits and revenues from applications developed).

In many cities around the globe FTTH/C plans are ongoing, often using lighting infrastructure to minimize the cost of the roll-out. This could also represent a strong boost to the development of smart applications.

An open and shared platform is one of the key elements to maximize smart city opportunities, as sharing capex and opex increases the profitability of each use case and enables a larger deployment. However, the current context tells a different story, particularly in the big cities: the majority of smart city initiatives are still represented by pilots in specific verticals.

In the following sections of the report we will focus on some of the possible “verticals”, outlining some quotes from different players.

Open Fiber, an Italian infrastructure operator, aims to bring ultra-wideband optical fiber to all the major cities in Italy and connect industrial areas, in order to build an ultra-wideband network that is as widespread and efficient as possible.

According to Open Fiber management, fiber roll-out plans are in progress in several countries, and the public lighting infrastructure is the preferred hosting infrastructure for fiber development thanks to capillarity and cost efficiency (lower €/meter compared to other network infrastructures or to digging).

In Italy, the “destinazioni d’uso” represent a potential roadblock for smart city services because utilities are often not allowed to use the poles for developing additional services (e.g., smart services), apart from street lighting, without an agreement with the municipality.

Open Fiber aims to enter the smart city value chain by developing connectivity infrastructure and providing connectivity O&M services.

Air quality and noise monitoring

The environmental topic is key both for government and municipalities, and it is increasingly attracting the attention of citizens:

- According to the WHO (World Health Organization), more than 80 percent of people living in urban areas are exposed to air-quality levels that exceed safe limits, and 4.2 million deaths every year are related to exposure to ambient (outdoor) air pollution.

- National and regional public entities and municipalities are responsible for keeping the natural environment under control, verifying compliance with environmental regulations and defining measures to close the gaps.

- Citizens can directly monitor the levels of pollution in their cities thanks to the increasing number of apps available in the market, such as AirVisual, BreezoMeter, Plume Air report, WideNoise and Airveda.

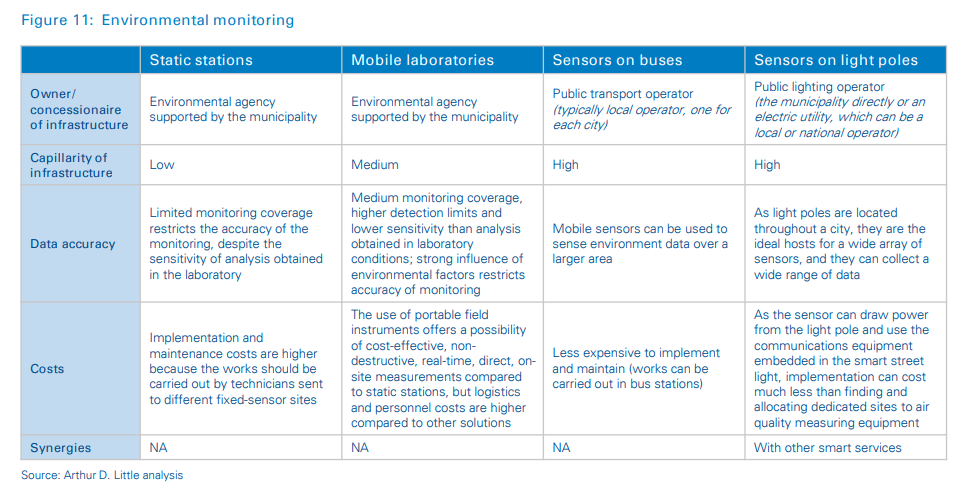

Environmental monitoring has historically been based on static and sparse measurement stations, but recently, many cities around the world have been adopting mobile laboratories to collect more granular data.

For instance, in Italy, ARPA Lombardia counts on only 150 stations in the Milan province and 106 mobile laboratories in the Lombardy region.

Across the Ile-de-France region there are 60 stations and mobile laboratories in specific areas or subjects of interest (such as airports, train stations and the Paris ring road), and 71 stations are set up in Washington DC.

Noise-monitoring sensors, apart from generating continuous, dense data on urban noise, provide significant data to support city-wide planning decisions such as traffic planning and school placement, as well as to inform and monitor public health initiatives related to environmental conditions.

Lamp poles, thanks to their widespread distribution, can easily host air and noise sensors: in fact, these sensors are constantly becoming smaller, without compromising reliability, and lighting poles may offer a cost-effective, quality service (e.g., more granular data) at a lower cost than other available solutions (See Figure 11).

The service developed for the municipality of Catania (currently been testing on other municipalities) implies the usage of city transports during their regular daily route in order to track the air quality in real time enabling on-the-edge IoT services for Smart City. The Mobile Sensing Station installed on the bus measures the level of pollutants along the route sending them to the Smart IoT platform through the TIM mobile radio network.

Data gathered and processed in cloud allow to create new services focused on several targets:

- Third parties (e.g. Startup): Application Programming Interface provided by TIM (B2B), aiming at launching new apps developing new business models

- Municipality: a web controlling dashboard to monitor the urban area air quality inside the Smart City Control Room

- Citizens: a mobile app that allows to receive green feedbacks/suggestions regard behaviors to be taken or not based on the level of pollution detected

Public safety and security

One of the main goals of governments and emergency services is to deliver safe, secure and sustainable cities (“safe city”), which requires several things:

- Integrated system

An infrastructure with common sensors connected by a shared network. Evolved from a disparate set of sensors with no interoperability

- Multi-agency collaboration

Moving beyond shared infrastructure to sharing intelligence, operational procedures and planning

- Situational awareness

Real-time information, with traffic data, sensor positions, resource locations, weather and other intelligence.

- Video data & analytics

Information collated from an array of city sensors and databases combined with video analytics, LPR, face recognition, behavioral analysis.

- Automated processes

All camera information is generated on one screen, alerts are registered, and the right operational procedure is generated.

Thanks to the Internet of Things (IoT) and connectivity services, safe city solutions enable governments and police departments to better protect their citizens from many threats; from terrorist attacks to natural disasters.

They also support other municipalities’ services, such as public health, fire and rescue, border control and social services.

The basic hardware of the safe city is the video camera, used for public video surveillance and video analysis to prevent crimes. It relies on prevention/detection/response/recovery processes such as facial recognition, object missing, and following, which constitute the value offering.

The business case for video analysis is strong, as connected video cameras allow a better service in terms of probability of detecting a crime, reaction time, and therefore security, at a lower cost.

The total cost, including devices and software for video analysis, is much lower compared to that of a control room.

Surveillance footage is captured in full-color HD and recorded in the cloud, where artificial intelligence processes can view and analyze the video.

In the event of something suspicious, alerts are sent to the appropriate personnel, while sophisticated facial recognition technology helps alert teams when a known shoplifter has entered the store or area. The use of AI systems will improve surveillance quality and reduce personnel effort.

In addition to the security issue, one of the main reasons for the growth of video surveillance services – and probably the most important – is the increase of wireless broadband networks.

This is due to its reliability, high quality and cost saving compared to wired connection (no digging work and less manpower).

On the other hand, some relevant constraints need to be evaluated as fragmentation of service buyers, privacy issues and the public sector as the main buyer, with its limited budgets and inflexible labor market. In B2B, buyers could be big video surveillance companies.

Even with these constraints, we expect that connected cameras will grow across countries, although as of today the market is still limited in size.

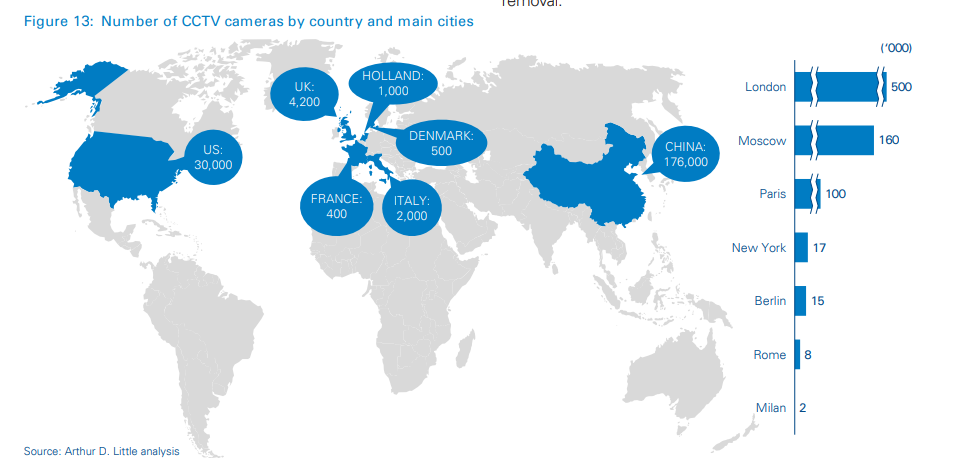

Moscow is a good example of implementation of a safe city: a network of about 150,000 cameras has been set up to monitor city streets, residents, businesses and visitors. Currently, the cameras are used for several purposes such as to ensure trash is picked up, to crack down on speeding and red-light running, to monitor the compliance of street advertising, and to track snow removal.

We asked Axxon – one of the world’s leading developers of video management and physical security information management software systems – if public poles could represent strategic infrastructure for development of smart services. The answer was “absolutely yes”, for the following reasons:

- The supply of electricity from the grid (even if it is not continuous, because there is energy saving in the objectives of efficient management). The pole can be controlled remotely or by local sensors; however, local control costs less.

- It can be connected to the fiber that guarantees broadband connectivity. Video surveillance takes advantage by backhauling compared to radio waves.

- It is an existing infrastructure – not very invasive, but widespread. It can be equipped with sensors that serve in other capacities. We consider that it takes a lot of cameras to guarantee the development of safe cities.

Below are use cases developed by some municipalities:

Digital advertising and communication (digital billboards)

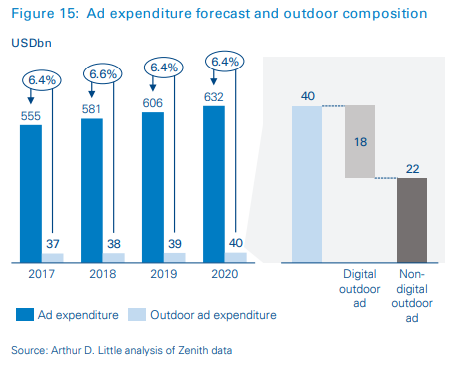

Outdoor advertising represents a limited part of global advertising expenditure, and could be divided into two macrosegments, digital and not digital, and where digital is expected to drive the growth of the market.

The main advantage of digital advertising is real-time campaigns (compared to the average time of 20 days for traditional billboards) and programmatic buying, thanks to connected signage that can be changed based on location, audience and time (overcoming the targeting limitation of traditional outdoor advertising).

Public lighting infrastructure can be used to host digital signage with the advantage of capillarity and potential cost synergies (sharing cost with other smart lighting services), although some restrictions remain, such as road safety regulation. One of the most relevant applications is in the medium-sized municipalities, which are characterized by saturation of traditional outdoor advertising media (municipal billboards), even if prices are typically lower than in urban centers.

Some use cases can be found on the following page.

Electric mobility

Only a decade ago, vehicles with batteries and electric motors felt like a distant sci-fi dream. Today, they are shaping the lives of consumers and the strategies of car producers, utilities and governments.

Arthur D. Little identified the following main trends:

- Production on a massive scale of new, compact forms of energy, such as lithium-ion batteries, will drive the adoption of electric mobility solutions.

- Urban mobility demand is booming – in terms of passengers-kilometers per year, it is set to double by 2050.

- Regulations will ban sales of cars with petrol and diesel combustion engines in the long term, and gradually replace them with alternative engines.

- The market for cars with electric engines is experiencing high growth: by 2025, there are expected to be 26.2 million electric vehicles.

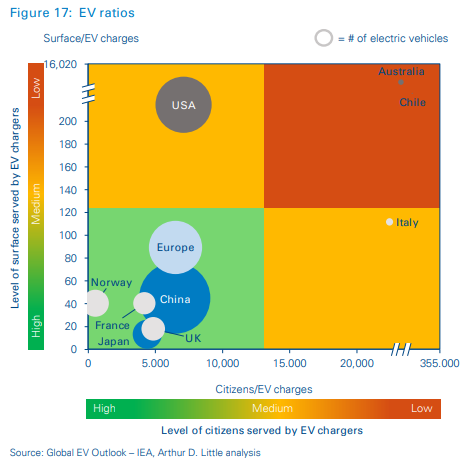

The global estimated number of EVs in 2016 was 2 million – a number led prominently by the US and China, with approximately half a million EVs each.

Currently, Japan has the best ratio of surface to EV charges (1 EV charge for 13 km²), and Norway has the best level of EV charges for citizens (1 EV charge for 535 citizens).

Chile, Australia and Italy have the worst levels of EV charges for citizens, but the total EV market for each country is lower than those of other countries.

The US, Australia and Chile have limited numbers of EV charges considering the extension of these countries.

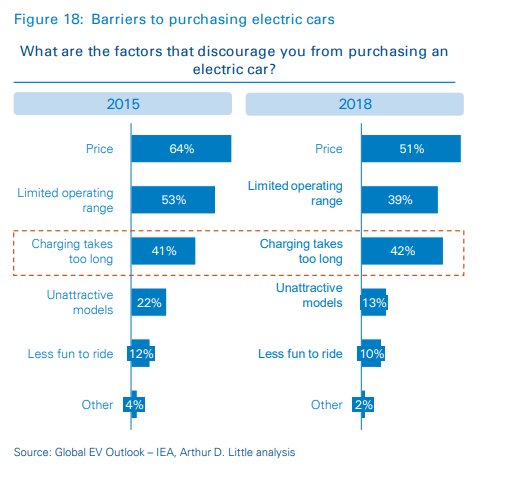

According to Arthur D. Little’s “Future of automotive mobility” survey, the potential of electric mobility is still limited by the price of electric cars compared to that of traditional-engine cars, as well as the shortcomings related to battery charging (operating range and charging time). Strong development of EV infrastructure would help to solve both operating-range and charging-time issues.

As the availability of charging stations represents a barrier to large-scale development, regulatory policies are trying to boost EV charger infrastructure roll-out. However, public options are typically limited to destination charging points, while electric vehicles are expected to be mostly charged at home, overnight. This is feasible for households with off-street parking, but more difficult for those without.

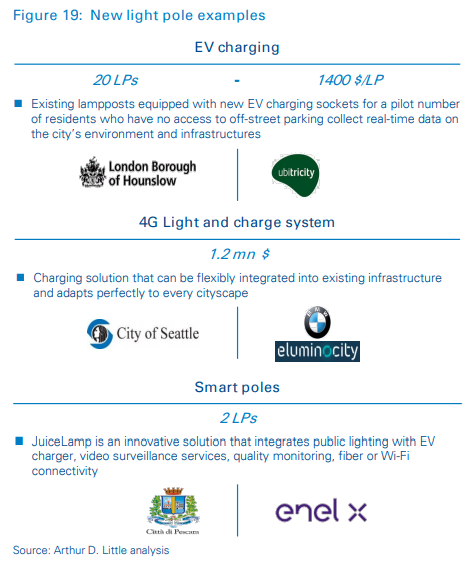

Some use cases, reported below, confirm Lamp-pole with EV charging station embedded, as a potential solution to dealing with charging point scarcity, enabling public access and reducing installation time and overall costs.

According to Nissan, a leading Japanese OEM, around 95 percent of EV charging will be at low speed, and smart poles could be a good solution to overcome cost barriers.

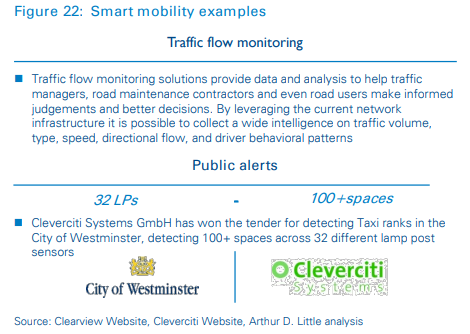

Smart mobility

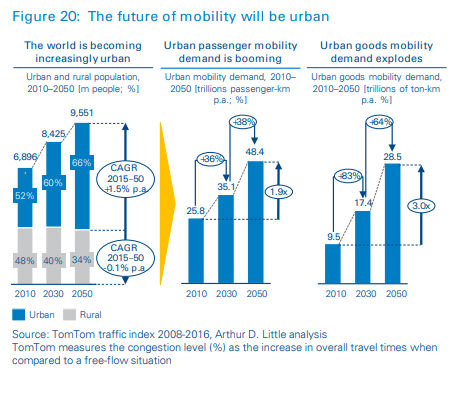

Mobility demand is booming. The mobility landscape is being reshaped, and urban mobility poses a massive challenge to metropolitan authorities and businesses, as well as great opportunities. The global demand for passenger mobility in urbanized areas – in terms of passengers to kilometers per year – is set to double by 2050. A supplementary factor affecting the traffic issue is the massive growth in the number of individual journeys taken daily since 2010, which puts increased pressure on existing urban mobility systems. Even larger growth is expected in the field of goods mobility, especially in dense urban areas, due to the growing importance of e-commerce and the accompanying boom in demand for last-mile delivery.

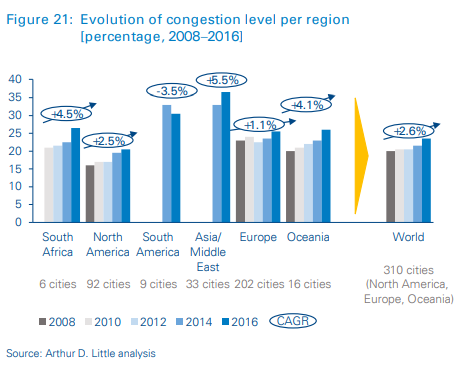

As a consequence, congestion is increasing.

Use of street lighting to monitor traffic flows can help to collect data about how people move, and the related patterns can influence driving mobility solutions and improve products such as parking guidance (real-time parking availability information and rates through other devices), parking enforcement (detection and reporting of payment, no-parking zones, optimum routes for enforcement officers), traffic monitoring and route planning.

Some use cases are found below

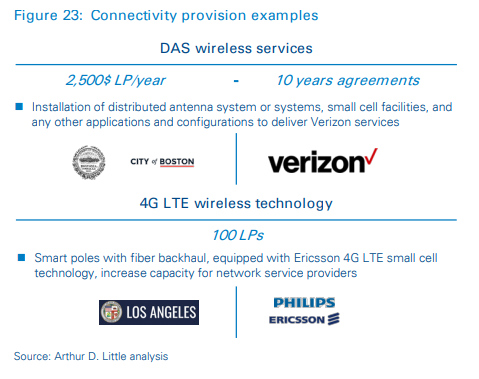

Connectivity provision

The new “smart pole” allows wireless carriers to quickly and easily densify their networks. In this case the pole will provide value-added services such as:

- Public/private wi-fi to local municipalities/dense urban areas through full fixed broadband connectivity (fiber).

- From just colocation to whole fiber connected radio base station to mobile/integrated telcos in order to increase capacity in urban areas, data offload and 5G microwave networks.

Therefore, the smart pole could be an important asset in 5G growth.

5G market: The first commercial launches were in Korea and the US in the first half of 2019. In five years global 5G subscribers are expected to reach 1 billion; 12 percent of all mobile subscriptions and 20 percent of mobile data traffic will be concentrated on this network.

Small cells: With 5G, small-cells demand will increase because, when network upgrades are no longer sufficient to support the increased traffic, operators will need to build new small cells. This demand growth will be remarkable in areas with IoT and smart city services, but weaker in other areas.

Light poles: Considering their distribution, light poles could be used to arrange small cells.

Some use cases can be found below.

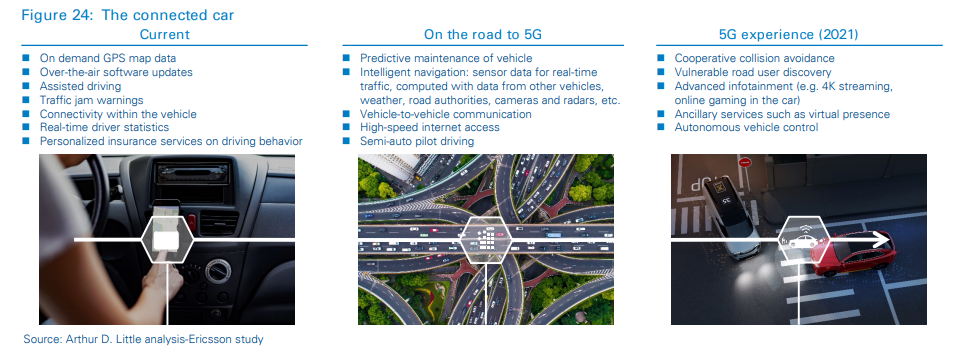

The connected car is one of the most interesting applications for 5G, as its features of reliability, latency, peak data rate and number of connected devices allow it to deploy the most advanced use cases, as highlighted in Figure 24.

Profitable business models still have to be defined and consolidated in order to maximize the benefits for all stakeholders involved. Different models have been observed around the world (revenue sharing, pure asset renting, partnership, etc.) but current price references still seem too high for large scaling application; this being an opportunity both for connectivity providers but also at the same time the asset owners.

3

Key takeaways and recommendations

Lighting poles represent strategic infrastructure for smart city development, thanks to their capillarity, connectivity and electrification. In particular:

- Poles’ capillarity is extremely relevant for video surveillance services and autonomous driving.

- Poles are the most convenient infrastructure on which to host a fiber network, and they can also be used for hosting small cells/antennas to meet 5G densification requirements.

- Poles are already equipped with electricity connection, and can host EV charging points with relevant cost benefits compared to traditional low-charge EV stations.

We observed a significant number of pilots emerging across countries, but a lack of large-scale deployment. The main constraints can be summarized as follows:

- Smart cities are still in an emerging phase and typically have gestation periods of 10–15 years before realizing their full GDP potential1 .

- Demand for smart city services is not yet sufficiently developed: players must create the need (e.g., as occurred for smart phones).

- The first buyer of smart cities is the public administration, which typically experiences financial constraints and lack of technical expertise:

- Players must engage the Public sector by designing a solution instead of trying to sell a product (e.g., using the project financing tool).

- Smart city solutions that enable cost efficiency are more likely to be pursued by municipalities (e.g., LED replacement is widely adopted in larger cities).

- Business models are not clearly defined and differ from one city to another. No smart city model can be observed universally.

- Several stakeholders are present and need to find the right way to collaborate.

.We recommend four steps for players which aim to grow in the smart city market:

- Map stakeholders and regulatory context:

- Map all stakeholders by sector and role (e.g., buyers versus regulators).

- Understand the regulatory framework and procurement processes.

- Prioritize and understand:

- Cluster stakeholders (e.g., public versus private, central versus local administration, buyers versus institutional, territorial reach) and prioritize based on a panel of key drivers (e.g., spending, smart maturity index, utilities’ presence in the municipality).

- Understand their priorities and how smart services can address them.

- Set different rules for engagement.

- Define the business model and set up strategic alliances:

- Understand own KSF and set up partnerships.

- Define the target position along the value chain (including offering a portfolio).

- Differentiate the positioning according to different types of municipalities (big versus small, mature versus immature, presence or not of a public utility owned by the municipality).

- Engage and monitor:

- Identify the target areas.

- Proactively engage key buyers (e.g., leveraging of project financing instrument).

- Effective institutional communication and lobby activities

- Monitor performance and identify areas of improvement.

DOWNLOAD THE FULL REPORT

22 min read • Energy, Utilities & Resources

The evolution of the street lighting market

What is its role in smart city development?

DATE

Executive Summary

The street lighting market is growing globally, boosted by regulatory policies that encourage energy efficiency, IoT convergence, LED price drops, and a new business model “as a service” in different industries. The new concept of “smart poles” is also growing around the world, with use cases that range from basic LED replacement and remote control to the more innovative concept of “smart poles” equipped to offer video surveillance services, air quality monitoring, fiber or Wi-fi connectivity (e.g., Enel’s JuiceLamp).

Public lighting infrastructure has three key features that position itself as potential strategic assets for smart cities’ concept, enabling the development of a common platform with significant cost synergies: capillarity, electrification and connectivity.

This study aims to analyze the main smart city services that can be developed leveraging public lighting infrastructure, identifying the main bottlenecks and roadblocks that prevent large-scale deployment and developing key recommendations for companies entering this new market. In order to do this, we analyzed a number of relevant use cases and interviewed different players along the value chain (Enel X, TIM, Open Fiber, Axxon, Arianna LED and two Italian municipalities). The main findings are summarized below:

- Lighting poles represent a strategic infrastructure for smart city development (and, in particular, for video-surveillance services and autonomous driving) thanks to their capillarity, connectivity and electrification.

- A significant number of pilot projects are emerging in many countries, but with a lack of large-scale deployment.

- The main constraints for large-scale development are related to a demand not yet in place (players need to create demand for smart services, and this takes time), main buyers (public administration) that have financial constraints and lack technical expertise, and the presence of several stakeholders that need to find the right way to collaborate.

- Public lighting operators need to innovate and push on technology innovation and new business models/partnerships to effectively leverage their infrastructure and participate in this new competition area.

1

Market overview and key drivers

Demand

Worldwide, there are around 320 million street lighting poles, with Asia accounting for 25 percent, Europe and North America for 20 percent and South America for 10 percent. Countries and municipalities differ in terms not only of sizing, but also LED penetration, capillarity and business models. The market is driven by several factors, among which are regulatory policies, IoT convergence, and LED price, in addition to the culture and morphology of each area.

Worldwide lighting density, in terms of urban population for each lighting point, is on average around 13, ranging from 7 European countries to over 20 in Asia-Pacific.

As of today, average LED penetration at a global level is still below 15 percent, with significant differences among countries. For example, Japan and Canada showed higher LED penetration rates (around 44-50 percent), while South America showed an average rate below 5 percent.

In Europe penetration is around 10 percent, with only Germany above, and in USA around 26 percent. Even within the same countries, LED penetration are quite different: some big cities have already reached 100 percent (e.g., Milan and New York), while small ones are still struggling, mainly with financial barriers.

The business case for switching to LED is already strong, as LED technology can generate savings of 50–80 percent of energy costs (which accounts for around 75 percent of total cost, while the other 25 percent is related to O&M).

This allows payback of the initial investment and generation of enough profits to cover the annual cost of lamp replacement.

Key drivers

Our study shows three key drivers which are boosting the development of smart street lighting:

- Regulatory policies: Policies encouraging the use of energyefficient lighting systems are also helping to propel market growth

- IoT convergence: Smart city development and advanced remote control systems drive the growth of the VAS segment.

- LED prices drop: Falling costs and improvement in quality are making LED the default option for lighting.

We asked Arianna LED – an Italian company specializing in the design and manufacture of LED lighting systems – what were the main constraints that players faced in “LED transitions” and why the transition process is slow:

- Complex regulation, with several entities engaged.

- Project sizing: a profitable business case requires a minimum of 20,000 street lighting points – potentially attractive to an energy service company (ESCo) aimed at mitigating municipalities’ upfront financial constraints.

- Political conflicts that prevent municipalities from collaborating to organize tenders and benefit from scale.

- Product requirements.

A recommended solution for small municipalities is to pool their decision-making and purchasing power in order to leverage economies of scale and access competitive LED replacement business cases (e.g., as 35 municipalities in southeastern Pennsylvania have done).

Regulatory policies

Smart street lighting projects represent a fast and relatively simple way to pursue emission and energy efficiency targets.

At the United Nations Climate Change Conference (COP 21) in Paris in December 2015, 195 countries adopted the first-ever universal, legally binding global climate deal. The agreement set out a global action plan to put the world on track to avoid dangerous climate change by limiting global warming to well below 2°C. To achieve this, the world must stop the growth in greenhouse gas emissions by 2020 and reduce them by 60 percent of 2010 levels by 2050. Furthermore, in 2016 the European Union published the Clean Energy for All Europeans rules, or so-called “Winter Package”, for reforming the European Union electricity market.

Since 2000 Europe has issued many directives about pollution, and after the Paris Agreement it developed different long-term plans, which included increasing targets in 2020, 2030 and 2050. 20 percent of the whole EU budget for 2014-2020 is spent on climate- related actions and the Commission has proposed raising this share to at least 25% for 2021-2027. In addition, on October 3, 2018 the European Parliament voted for a 20 percent cut in CO2 emissions from new cars and vans in 2025, as well as a 40 percent reduction in 2030, in a bid to speed up Europe’s electric car revolution. At the end of 2018, the European Commission defined a vision for a modern, competitive, prosperous and climate-neutral economy, aiming at achieving net-zero greenhouse gas emissions by 2050 through a socially fair, cost-efficient transition (Comm. 773/2018).

In 2017 the US administration decided unilaterally to stay out of the Paris Agreement. The US is one of the very few large, energy-consuming economies that do not have national energy reduction targets in place, although it has adopted stringent energy codes for new buildings.

Canada showed strong commitment to GHG emission reduction with a target of 17 percent below 2005 levels by 2020 and 30 percent by 2030, equivalent to 607 megatons as defined by Canada’s original 2005 baseline. In addition, several energy efficiency initiatives have been defined at either province or federal level on a sector-by-sector basis.

Other local or national initiatives have been promoted by several countries in the far east and Asia, setting ambitious targets in terms of energy efficiency.

South Korea’s second National Energy Master Plan established a goal of 13 percent below the business-as-usual emission level by 2035. It also implemented various regulations, including a plan for an emissions-trading system (financial support and tax credits).

China launched many initiatives in the run-up to COP 21, and developed its climate diplomacy, showing strong improvement in terms of energy intensity. This included a new emission trading system aimed at reducing carbon, which should be up and running in 2019.

IoT convergence

The Internet of Things is the connection of everyday products such as cars, alarm clocks, and lights to computing devices via the internet to allow them to exchange data. Street lighting will benefit from this, as lighting poles will become hosting infrastructure for several connected devices (e.g., sensors, video cameras, EV chargers)

As reported in Figure 6, in 2024 there will be 22 billion connected IoT devices, with an average IoT devices CAGR (wide-area and short-range) of 17 percent.

LED prices drop

LED prices are expected to strongly decrease in the medium to long term (up to 70 percent by 2050 for USA as reported in Figure 7) and high-quality products (e.g., RGB W) which are able to provide different light temperatures and new services (e.g., adaptive lighting) have been placed on the market.

Value chain and main players

Technology is deeply changing the lighting market, making it into a new booster/enabler for smart city development. However, as a consequence, complexity of the sector’s value chain is increasing and new players are entering the market, as reported in Figure 8.

Utilities typically manage public lighting services, acquiring light lamps from manufacturers, developing O&M services, and defining service-level agreements and related remuneration with municipalities. Now the value chain is changing, with new players entering the market and new partnerships arising. (These include, for example, telco operators that provide connectivity; LED manufactures that, in addition to lamps, are developing their own IOT platforms; vertical players that provide solutions such as EV charging stations and video surveillance services).

Enel X is a global company belonging to the Enel Group with a long-standing experience in installation, operation and maintenance of traditional public lighting. The company is currently focusing its efforts on transitioning the existing asset base to more efficient technology, as well as providing technologically and digitally advanced solutions to B2G customers (municipalities and the like) to support a ‘smart’ urban environment in key application areas in public lighting, mobility, fiber optic-based connectivity, and urban resilience.

As a perfect example of technology integration, efficiency and innovation, Enel X has developed Juice Lamp, an innovative product that combines the latest available lighting technology with two chargers for electric vehicles. The design is attractive and can be adapted to any urban context thanks to its 4 differentiated pole styles.

Features:

- LED light pole combined with remote controlling technology and option to install adaptive lighting features.

- Two integrated chargers with capacity of up to 22kW each, by no means equal to the public standing technology offered by Enel X.

Benefits:

- It can be fitted to any street environment thanks to its range of heights, colors and design: there are 3 ‘modern’ styles plus a ‘classic’ one that fits well within historic sections of cities, or for towns with a specific sensitivity in this area.

- Quick charging, thanks to the Juice Box connectors which each have a capacity of 22kW.

- Interoperability with other potential mobility service providers and possibility to couple any street lighting devices.

- Possibility to integrate video surveillance, traffic analytics, environmental monitoring, connectivity, other smart services.

Scope

With no specific constraint or limitation to its implementation, Enel X has also developed an innovative tool ‘YoUrban©’, a single platform with a twofold application: a mobile app for city-based individuals and a web-based management tool for municipalities.

YoUrban© allows individuals to promptly and easily alert municipalities about lighting points malfunctioning (whose identification is easy thanks to a GPS system) while following any ensuing development, sharing the positive outcome of the maintenance activities on social media, getting access to a section including ‘news’ and earn rewarding points that can be utilized following instructions included in the app.

At the same time, municipalities get an advantage in terms of faster and more cost-effective management of maintenance activities given that the portal allows a fully digitalized experience of activities like, amongst others: i) getting dashboards showing the most relevant key performance indicators about the level of quality of the public lighting system; ii) monitoring of closed/open incidents for urgent interventions, iii) visualization ‘on map’ of the assets under management and customizable statistics about the number of reported incidents, average closing time, etc., iv) direct connection with any related call center and engineers; v) direct connection with suppliers and option to accept online offers and cost estimations for the maintenance and repair activities offered by Enel X.

2

The smart revolution

Public lighting infrastructure has three key features that position it as a potential strategic asset for smart city development: capillarity, electrification and connectivity.

Finding new revenue streams implies clear understanding of enablers, constraints and a successful business model.

Arthur D. Little’s “Smart city framework” includes the key pillars to help municipalities leverage their street lighting infrastructure to successfully set up and implement strategies that will transform them into smart cities.

Several cities have already implemented connected LED streetlights using different technologies depending on the smart city’s applications. (Examples include the IEEE 802.15.4g wireless RF mesh architecture used in Miami and Paris, as well as the combination of Vodafone machine-to-machine SIM cards with Vodafone’s M2M wireless network, which was adopted in Los Angeles and Jakarta.)

One of the main infrastructure challenges is to balance the network capacity requirement against the different smart city applications (cost of network roll-out versus benefits and revenues from applications developed).

In many cities around the globe FTTH/C plans are ongoing, often using lighting infrastructure to minimize the cost of the roll-out. This could also represent a strong boost to the development of smart applications.

An open and shared platform is one of the key elements to maximize smart city opportunities, as sharing capex and opex increases the profitability of each use case and enables a larger deployment. However, the current context tells a different story, particularly in the big cities: the majority of smart city initiatives are still represented by pilots in specific verticals.

In the following sections of the report we will focus on some of the possible “verticals”, outlining some quotes from different players.

Open Fiber, an Italian infrastructure operator, aims to bring ultra-wideband optical fiber to all the major cities in Italy and connect industrial areas, in order to build an ultra-wideband network that is as widespread and efficient as possible.

According to Open Fiber management, fiber roll-out plans are in progress in several countries, and the public lighting infrastructure is the preferred hosting infrastructure for fiber development thanks to capillarity and cost efficiency (lower €/meter compared to other network infrastructures or to digging).

In Italy, the “destinazioni d’uso” represent a potential roadblock for smart city services because utilities are often not allowed to use the poles for developing additional services (e.g., smart services), apart from street lighting, without an agreement with the municipality.

Open Fiber aims to enter the smart city value chain by developing connectivity infrastructure and providing connectivity O&M services.

Air quality and noise monitoring

The environmental topic is key both for government and municipalities, and it is increasingly attracting the attention of citizens:

- According to the WHO (World Health Organization), more than 80 percent of people living in urban areas are exposed to air-quality levels that exceed safe limits, and 4.2 million deaths every year are related to exposure to ambient (outdoor) air pollution.

- National and regional public entities and municipalities are responsible for keeping the natural environment under control, verifying compliance with environmental regulations and defining measures to close the gaps.

- Citizens can directly monitor the levels of pollution in their cities thanks to the increasing number of apps available in the market, such as AirVisual, BreezoMeter, Plume Air report, WideNoise and Airveda.

Environmental monitoring has historically been based on static and sparse measurement stations, but recently, many cities around the world have been adopting mobile laboratories to collect more granular data.

For instance, in Italy, ARPA Lombardia counts on only 150 stations in the Milan province and 106 mobile laboratories in the Lombardy region.

Across the Ile-de-France region there are 60 stations and mobile laboratories in specific areas or subjects of interest (such as airports, train stations and the Paris ring road), and 71 stations are set up in Washington DC.

Noise-monitoring sensors, apart from generating continuous, dense data on urban noise, provide significant data to support city-wide planning decisions such as traffic planning and school placement, as well as to inform and monitor public health initiatives related to environmental conditions.

Lamp poles, thanks to their widespread distribution, can easily host air and noise sensors: in fact, these sensors are constantly becoming smaller, without compromising reliability, and lighting poles may offer a cost-effective, quality service (e.g., more granular data) at a lower cost than other available solutions (See Figure 11).

The service developed for the municipality of Catania (currently been testing on other municipalities) implies the usage of city transports during their regular daily route in order to track the air quality in real time enabling on-the-edge IoT services for Smart City. The Mobile Sensing Station installed on the bus measures the level of pollutants along the route sending them to the Smart IoT platform through the TIM mobile radio network.

Data gathered and processed in cloud allow to create new services focused on several targets:

- Third parties (e.g. Startup): Application Programming Interface provided by TIM (B2B), aiming at launching new apps developing new business models

- Municipality: a web controlling dashboard to monitor the urban area air quality inside the Smart City Control Room

- Citizens: a mobile app that allows to receive green feedbacks/suggestions regard behaviors to be taken or not based on the level of pollution detected

Public safety and security

One of the main goals of governments and emergency services is to deliver safe, secure and sustainable cities (“safe city”), which requires several things:

- Integrated system

An infrastructure with common sensors connected by a shared network. Evolved from a disparate set of sensors with no interoperability

- Multi-agency collaboration

Moving beyond shared infrastructure to sharing intelligence, operational procedures and planning

- Situational awareness

Real-time information, with traffic data, sensor positions, resource locations, weather and other intelligence.

- Video data & analytics

Information collated from an array of city sensors and databases combined with video analytics, LPR, face recognition, behavioral analysis.

- Automated processes

All camera information is generated on one screen, alerts are registered, and the right operational procedure is generated.

Thanks to the Internet of Things (IoT) and connectivity services, safe city solutions enable governments and police departments to better protect their citizens from many threats; from terrorist attacks to natural disasters.

They also support other municipalities’ services, such as public health, fire and rescue, border control and social services.

The basic hardware of the safe city is the video camera, used for public video surveillance and video analysis to prevent crimes. It relies on prevention/detection/response/recovery processes such as facial recognition, object missing, and following, which constitute the value offering.

The business case for video analysis is strong, as connected video cameras allow a better service in terms of probability of detecting a crime, reaction time, and therefore security, at a lower cost.

The total cost, including devices and software for video analysis, is much lower compared to that of a control room.

Surveillance footage is captured in full-color HD and recorded in the cloud, where artificial intelligence processes can view and analyze the video.

In the event of something suspicious, alerts are sent to the appropriate personnel, while sophisticated facial recognition technology helps alert teams when a known shoplifter has entered the store or area. The use of AI systems will improve surveillance quality and reduce personnel effort.

In addition to the security issue, one of the main reasons for the growth of video surveillance services – and probably the most important – is the increase of wireless broadband networks.

This is due to its reliability, high quality and cost saving compared to wired connection (no digging work and less manpower).

On the other hand, some relevant constraints need to be evaluated as fragmentation of service buyers, privacy issues and the public sector as the main buyer, with its limited budgets and inflexible labor market. In B2B, buyers could be big video surveillance companies.

Even with these constraints, we expect that connected cameras will grow across countries, although as of today the market is still limited in size.

Moscow is a good example of implementation of a safe city: a network of about 150,000 cameras has been set up to monitor city streets, residents, businesses and visitors. Currently, the cameras are used for several purposes such as to ensure trash is picked up, to crack down on speeding and red-light running, to monitor the compliance of street advertising, and to track snow removal.

We asked Axxon – one of the world’s leading developers of video management and physical security information management software systems – if public poles could represent strategic infrastructure for development of smart services. The answer was “absolutely yes”, for the following reasons:

- The supply of electricity from the grid (even if it is not continuous, because there is energy saving in the objectives of efficient management). The pole can be controlled remotely or by local sensors; however, local control costs less.

- It can be connected to the fiber that guarantees broadband connectivity. Video surveillance takes advantage by backhauling compared to radio waves.

- It is an existing infrastructure – not very invasive, but widespread. It can be equipped with sensors that serve in other capacities. We consider that it takes a lot of cameras to guarantee the development of safe cities.

Below are use cases developed by some municipalities:

Digital advertising and communication (digital billboards)

Outdoor advertising represents a limited part of global advertising expenditure, and could be divided into two macrosegments, digital and not digital, and where digital is expected to drive the growth of the market.

The main advantage of digital advertising is real-time campaigns (compared to the average time of 20 days for traditional billboards) and programmatic buying, thanks to connected signage that can be changed based on location, audience and time (overcoming the targeting limitation of traditional outdoor advertising).

Public lighting infrastructure can be used to host digital signage with the advantage of capillarity and potential cost synergies (sharing cost with other smart lighting services), although some restrictions remain, such as road safety regulation. One of the most relevant applications is in the medium-sized municipalities, which are characterized by saturation of traditional outdoor advertising media (municipal billboards), even if prices are typically lower than in urban centers.

Some use cases can be found on the following page.

Electric mobility

Only a decade ago, vehicles with batteries and electric motors felt like a distant sci-fi dream. Today, they are shaping the lives of consumers and the strategies of car producers, utilities and governments.

Arthur D. Little identified the following main trends:

- Production on a massive scale of new, compact forms of energy, such as lithium-ion batteries, will drive the adoption of electric mobility solutions.

- Urban mobility demand is booming – in terms of passengers-kilometers per year, it is set to double by 2050.

- Regulations will ban sales of cars with petrol and diesel combustion engines in the long term, and gradually replace them with alternative engines.

- The market for cars with electric engines is experiencing high growth: by 2025, there are expected to be 26.2 million electric vehicles.

The global estimated number of EVs in 2016 was 2 million – a number led prominently by the US and China, with approximately half a million EVs each.

Currently, Japan has the best ratio of surface to EV charges (1 EV charge for 13 km²), and Norway has the best level of EV charges for citizens (1 EV charge for 535 citizens).

Chile, Australia and Italy have the worst levels of EV charges for citizens, but the total EV market for each country is lower than those of other countries.

The US, Australia and Chile have limited numbers of EV charges considering the extension of these countries.

According to Arthur D. Little’s “Future of automotive mobility” survey, the potential of electric mobility is still limited by the price of electric cars compared to that of traditional-engine cars, as well as the shortcomings related to battery charging (operating range and charging time). Strong development of EV infrastructure would help to solve both operating-range and charging-time issues.

As the availability of charging stations represents a barrier to large-scale development, regulatory policies are trying to boost EV charger infrastructure roll-out. However, public options are typically limited to destination charging points, while electric vehicles are expected to be mostly charged at home, overnight. This is feasible for households with off-street parking, but more difficult for those without.

Some use cases, reported below, confirm Lamp-pole with EV charging station embedded, as a potential solution to dealing with charging point scarcity, enabling public access and reducing installation time and overall costs.

According to Nissan, a leading Japanese OEM, around 95 percent of EV charging will be at low speed, and smart poles could be a good solution to overcome cost barriers.

Smart mobility

Mobility demand is booming. The mobility landscape is being reshaped, and urban mobility poses a massive challenge to metropolitan authorities and businesses, as well as great opportunities. The global demand for passenger mobility in urbanized areas – in terms of passengers to kilometers per year – is set to double by 2050. A supplementary factor affecting the traffic issue is the massive growth in the number of individual journeys taken daily since 2010, which puts increased pressure on existing urban mobility systems. Even larger growth is expected in the field of goods mobility, especially in dense urban areas, due to the growing importance of e-commerce and the accompanying boom in demand for last-mile delivery.

As a consequence, congestion is increasing.

Use of street lighting to monitor traffic flows can help to collect data about how people move, and the related patterns can influence driving mobility solutions and improve products such as parking guidance (real-time parking availability information and rates through other devices), parking enforcement (detection and reporting of payment, no-parking zones, optimum routes for enforcement officers), traffic monitoring and route planning.

Some use cases are found below

Connectivity provision

The new “smart pole” allows wireless carriers to quickly and easily densify their networks. In this case the pole will provide value-added services such as:

- Public/private wi-fi to local municipalities/dense urban areas through full fixed broadband connectivity (fiber).

- From just colocation to whole fiber connected radio base station to mobile/integrated telcos in order to increase capacity in urban areas, data offload and 5G microwave networks.

Therefore, the smart pole could be an important asset in 5G growth.

5G market: The first commercial launches were in Korea and the US in the first half of 2019. In five years global 5G subscribers are expected to reach 1 billion; 12 percent of all mobile subscriptions and 20 percent of mobile data traffic will be concentrated on this network.

Small cells: With 5G, small-cells demand will increase because, when network upgrades are no longer sufficient to support the increased traffic, operators will need to build new small cells. This demand growth will be remarkable in areas with IoT and smart city services, but weaker in other areas.

Light poles: Considering their distribution, light poles could be used to arrange small cells.

Some use cases can be found below.

The connected car is one of the most interesting applications for 5G, as its features of reliability, latency, peak data rate and number of connected devices allow it to deploy the most advanced use cases, as highlighted in Figure 24.

Profitable business models still have to be defined and consolidated in order to maximize the benefits for all stakeholders involved. Different models have been observed around the world (revenue sharing, pure asset renting, partnership, etc.) but current price references still seem too high for large scaling application; this being an opportunity both for connectivity providers but also at the same time the asset owners.

3

Key takeaways and recommendations

Lighting poles represent strategic infrastructure for smart city development, thanks to their capillarity, connectivity and electrification. In particular:

- Poles’ capillarity is extremely relevant for video surveillance services and autonomous driving.

- Poles are the most convenient infrastructure on which to host a fiber network, and they can also be used for hosting small cells/antennas to meet 5G densification requirements.

- Poles are already equipped with electricity connection, and can host EV charging points with relevant cost benefits compared to traditional low-charge EV stations.

We observed a significant number of pilots emerging across countries, but a lack of large-scale deployment. The main constraints can be summarized as follows:

- Smart cities are still in an emerging phase and typically have gestation periods of 10–15 years before realizing their full GDP potential1 .

- Demand for smart city services is not yet sufficiently developed: players must create the need (e.g., as occurred for smart phones).

- The first buyer of smart cities is the public administration, which typically experiences financial constraints and lack of technical expertise:

- Players must engage the Public sector by designing a solution instead of trying to sell a product (e.g., using the project financing tool).

- Smart city solutions that enable cost efficiency are more likely to be pursued by municipalities (e.g., LED replacement is widely adopted in larger cities).

- Business models are not clearly defined and differ from one city to another. No smart city model can be observed universally.

- Several stakeholders are present and need to find the right way to collaborate.

.We recommend four steps for players which aim to grow in the smart city market:

- Map stakeholders and regulatory context:

- Map all stakeholders by sector and role (e.g., buyers versus regulators).

- Understand the regulatory framework and procurement processes.

- Prioritize and understand:

- Cluster stakeholders (e.g., public versus private, central versus local administration, buyers versus institutional, territorial reach) and prioritize based on a panel of key drivers (e.g., spending, smart maturity index, utilities’ presence in the municipality).

- Understand their priorities and how smart services can address them.

- Set different rules for engagement.

- Define the business model and set up strategic alliances:

- Understand own KSF and set up partnerships.

- Define the target position along the value chain (including offering a portfolio).

- Differentiate the positioning according to different types of municipalities (big versus small, mature versus immature, presence or not of a public utility owned by the municipality).

- Engage and monitor:

- Identify the target areas.

- Proactively engage key buyers (e.g., leveraging of project financing instrument).

- Effective institutional communication and lobby activities

- Monitor performance and identify areas of improvement.

DOWNLOAD THE FULL REPORT